Should you invest only if you’re debt free?

One of the biggest financial conundrums is whether to invest the extra cash you have at the end of the month into your savings or use it to pay off outstanding debts. The latter can be tempting as unpaid debt accumulates interest charges that only add to the total balance you need to pay off.

One of the biggest financial conundrums is whether to invest the extra cash you have at the end of the month into your savings or use it to pay off outstanding debts. The latter can be tempting as unpaid debt accumulates interest charges that only add to the total balance you need to pay off.

However, investing in bonds, mutual funds, stocks, or a retirement fund lets you put money aside and accumulate positive interest. So it’s crucial to understand the pros and cons of paying off debt and investing your hard-earned cash.

Pros of paying down debt

Paying down your debt can be a better option than investing your money in some situations. These include:

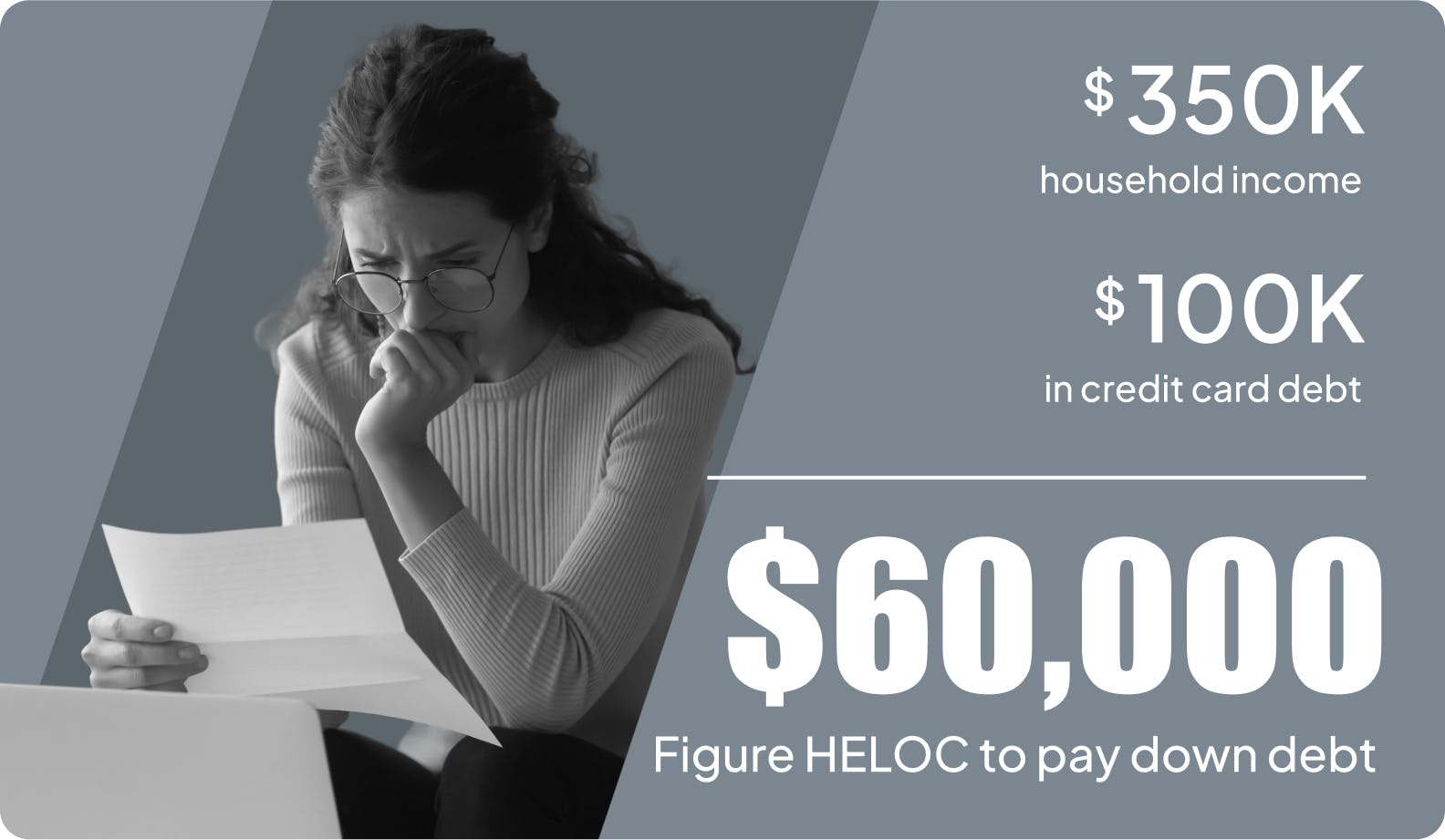

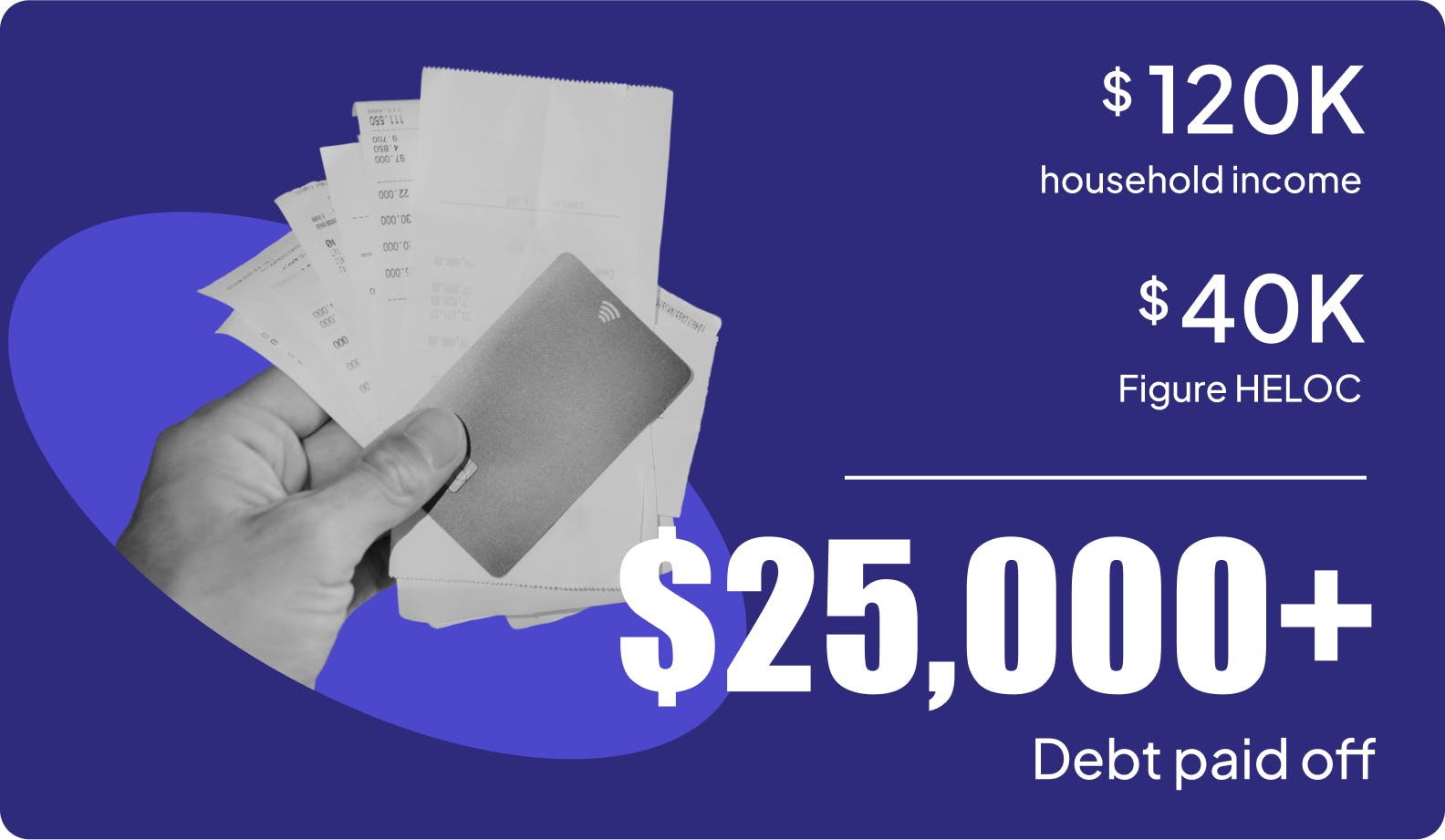

High interest rates: Some forms of debt, like credit cards, typically have an interest rate that could be higher than the interest you’d stand to earn on any investment you make. For example, the average APR on credit cards is over 20%, while the typical return on stock market investments is about 10%. These high interest rates can make it challenging to pay off the total balance of your debt and result in you losing money in the long run. Therefore, if you have credit card debt, you should prioritize removing the burden of high interest rates. Other forms of debt, including mortgages and student loans, tend to have relatively lower interest rates, which makes it less necessary to pay them off as quickly as possible.

Boosting credit score: A low credit score can result in your paying higher interest rates and even being refused a loan, a rental property, or hired for a job. Your credit score is calculated through your credit utilization rate, which divides the amount of revolving credit you use by the total credit available across your accounts. Lenders prefer you to have a credit utilization rate of 30% or below, which signifies you only use the credit you need and have available credit. Amassing a large debt can negatively impact your credit score as it tells lenders you’re incapable of managing your finances or you’ve borrowed above your means. So paying off a large debt can help you boost your credit score and reduce your interest rates for future credit applications.

Peace of mind: Having a vast amount of debt can significantly impact your life. If your outstanding debts are causing you concern, then it could be best to pay them off, regardless of whether you’ll get a better return by investing.

Pros of investing

Investing your money can help you grow your savings by securing a better interest rate than those on your outstanding debts.

Higher interest rates: It makes sense to invest your money if you can earn more interest than you’re incurring on your debts. For example, if you have a mortgage with a 4% interest rate and a stock market index fund that offers 10% annual returns, it’s a better long-term financial option to invest your money. Playing the stock market via the growing list of mobile apps can appear exciting, but it’s easy to quickly lose your money if you don’t know what you’re doing. So set limits on your spending and ensure you meet your committed payments before investing that money.

Risk tolerance: Another factor to weigh into your decision is psychological. If you’re comfortable taking the gamble to invest, knowing that your funds could fluctuate in value as the markets adjust, then you’re a good candidate for various investment opportunities. If, however, you might worry about how the markets flow up and down, you may want to consider other options.

Other factors to consider

When considering whether to invest or pay off your debts, it’s essential to bear in mind other factors like the economic climate, fluctuating rates, and more.

Fluctuating rates: If you decide investment is the best way forward, you need to consider their volatile nature. Most funds have fluctuating interest rates, meaning an inviting-looking 10% interest rate could drop dramatically over the course of a year. Likewise, if you decide not to pay off a debt, you could find lenders decide to charge you a higher interest rate.

Tax considerations: Some forms of debt offer tax benefits. For example, the interest you pay on a student loan and some mortgage interest can be deductible. So it’s advisable to consult a tax professional for more information.

How to pay off debt: If you have a lump sum fee to cover an outstanding loan then it’s relatively simple to pay off your debts. But if you have a smaller amount available, you’ll need to prioritize debts with higher interest rates. When it comes to credit card debt, you can transfer balances to a card with lower interest rates then pay them off. Some credit cards offer a promotional period that provides 0% interest for a certain period, which could help you pay off your debt without incurring interest.

Alternative strategies

Paying down your debt and investing your cash doesn’t have to be a one or the other choice. It can be advantageous to do both, setting aside money for an emergency fund while using some cash to pay off outstanding debts.

Emergency fund: An emergency fund can help you pay off unexpected costs like medical bills or home repair projects. You should look for an investment fund that’s low-risk and highly liquid, which means it offers quick and easy access to your money.

Debt consolidation loan: A debt consolidation loan allows you to borrow enough money to pay off existing debts and ensures you only have one outstanding debt to worry about, potentially at a lower interest rate.

Refinancing: Your decision to pay off a debt or invest can be affected by the option to refinance at a lower rate or secure a 0% interest promotion. Refinancing enables you to reduce interest rate costs, reduce monthly debt payments, and increase your savings rate. This can offer current and future benefits but requires discipline not to spend the credit on your existing lines of credit.

Retirement funds: Most companies offer retirement funds that are a great option for building savings. They provide a matching arrangement, like a 401(k) match, in which your employer commits a percentage of your investment. For example, if your employer pays 50 cents for every $1 you invest into your retirement fund, that’s an immediate 50% return. As a result, this high return rate is prioritized by most financial advisors.

Receiving a windfall: When you receive a windfall like a work bonus or inheritance money you face a big decision over how to use that money. You could set aside a sizeable emergency fund or split cash evenly between your debt and a new investment. But if you have a significant debt with high interest rates, you may want to focus on paying it off to reduce your monthly repayments.

Figure out your finances

The decision over whether to use a lump sum to pay off debts or begin a new investment opportunity depends on a range of factors. If you have a significant outstanding debt accruing high interest then it’s advisable to prioritize removing it. That said, if you do have outstanding debts, it doesn’t have to be a barrier to investing your money.

Figure makes it easy to get your debt under control by providing consumers fast and easy lending options. Our best-in-class technology helps you access and maximize your assets and make the right investment options for your specific financial situation.