The Homeowner’s Complete Guide to Debt Consolidation

One solution to high-interest-rate debts is to refinance with a new loan — one that will save you money, reduce your risk, or both.

It’s easy to end up in debt. You’re not alone.

Take healthcare, for example. Individuals and families face higher deductibles, rising premiums, and a freelance economy where individuals are increasingly responsible for their own insurance coverage. When health issues arise, you need to take care of yourself and your family, but you may walk away with thousands of dollars on your credit card — out of the blue. And it’s not just healthcare.

Add student loans or a mortgage to the mix, and it’s no wonder debt can creep up. But you can turn the tide.

What is debt consolidation?

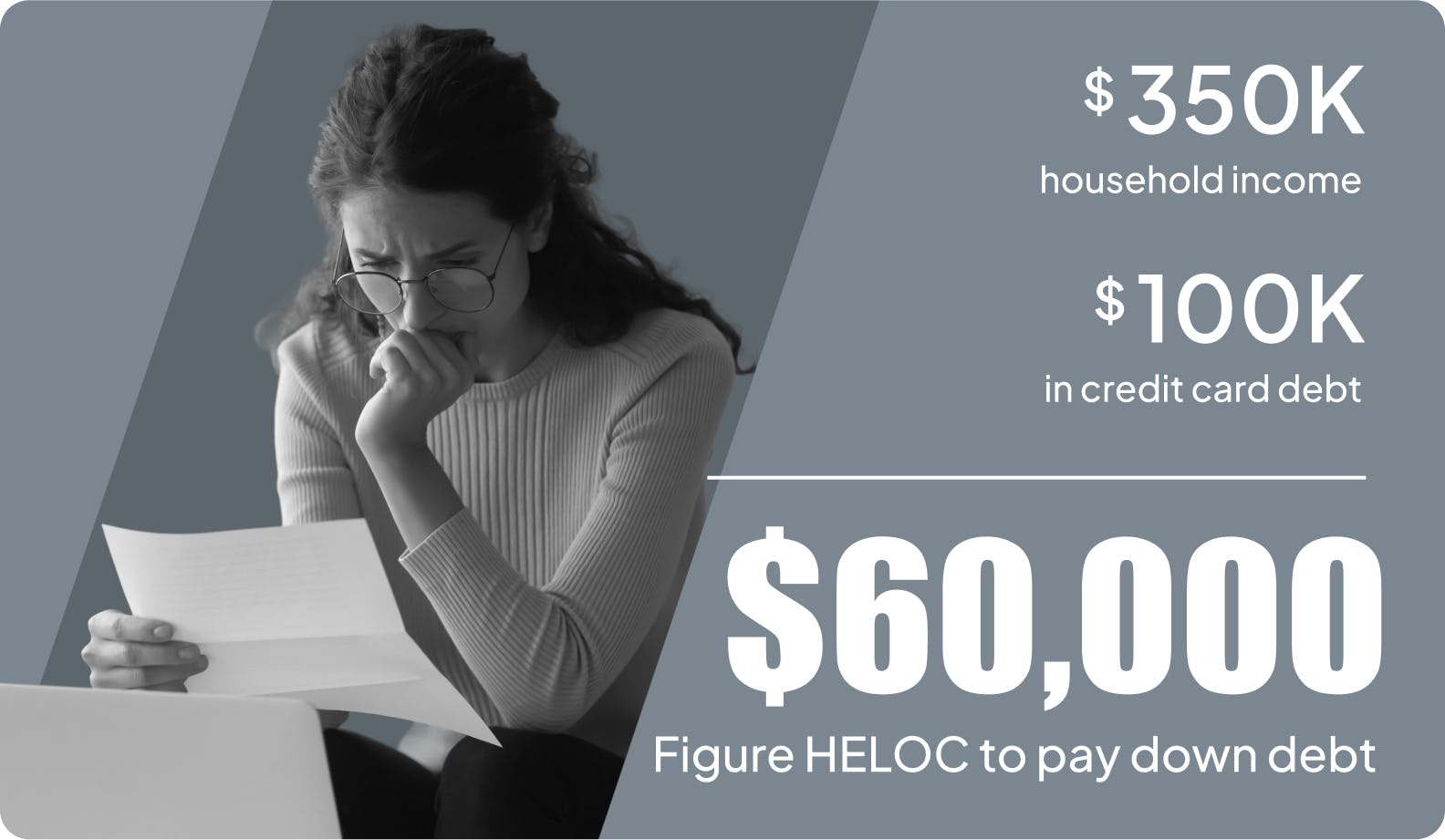

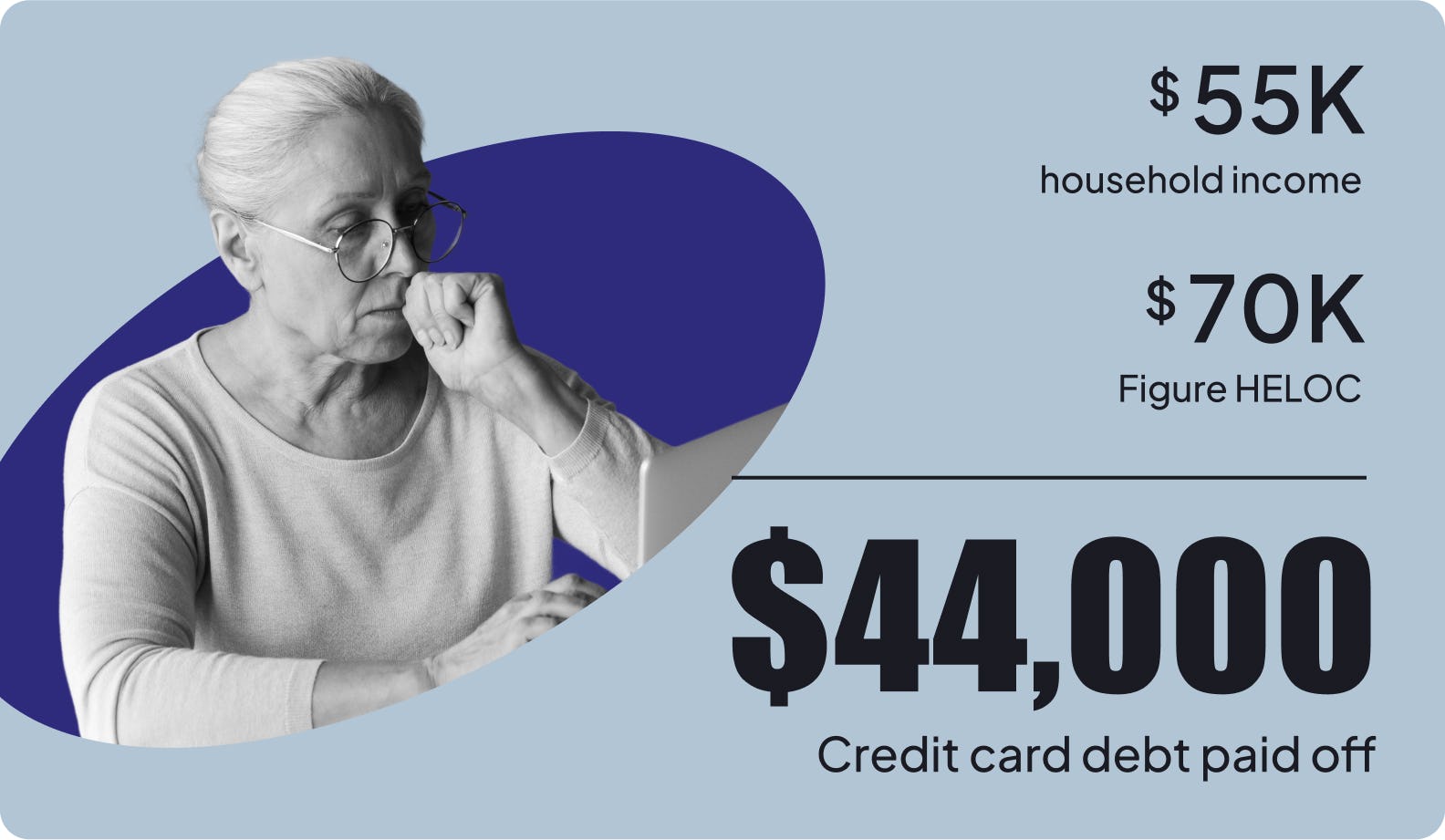

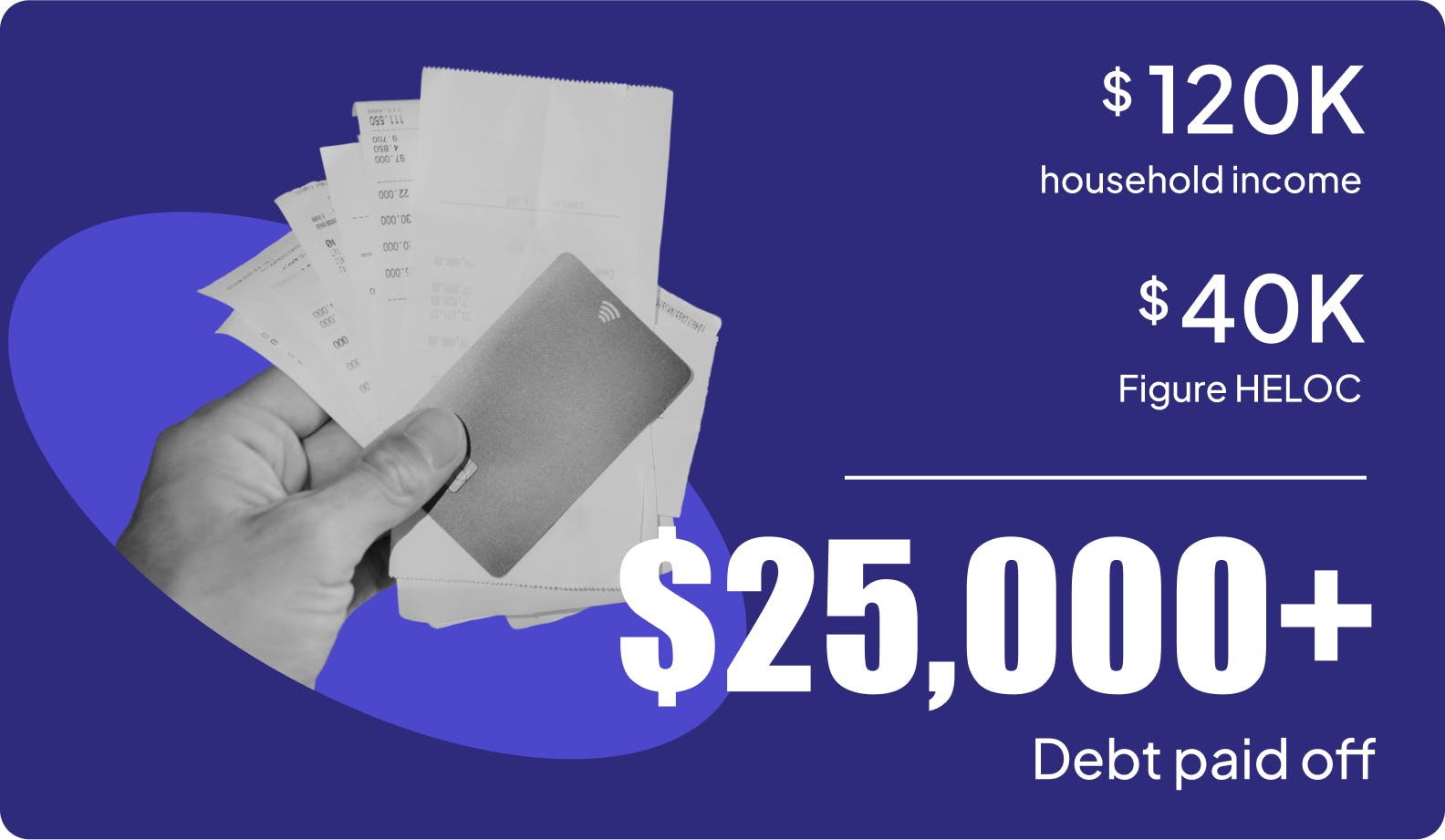

Debt consolidation is a way to refinance your debt by taking out one loan to pay off the others. The most common ways to consolidate your debt are with a personal loan or 0% balance transfer credit card. But homeowners have a huge advantage in consolidating debt that others don’t – home equity loans. They often will have a lower interest rate with an ability to pay over a longer period of time.

How does debt consolidation work?

There are two very common ways to consolidate debt, both of which concentrate your payments into one monthly bill:

Get a 0% interest, balance-transfer credit card. Then transfer all your debt onto this card and pay the balance in full during the promotional period, which is usually 9 -12 months.

Get a fixed-rate debt consolidation loan, then use the money from the loan to pay off your debt. Ideally this loan has a lower interest rate, so you can then pay back the loan in installments over a set amount of time.

But if you’re a homeowner, there’s a better option. A home equity line of credit will allow you to consolidate your debt while providing you with a much lower interest rate than credit cards or personal loans. Home equity loans use your home as collateral, which is why they’re able to offer lower interest rates.

What are the pros of debt consolidation?

Makes it easier to reach your financial goals - Without burdensome debt payments, it’s easier to work toward financial goals. For example, you may want to save for retirement, travel, pay for education, or give more to charity.

More freedom to choose - Sometimes debt feels like a trap and sometimes it actually leaves you trapped. When you pay a significant amount on consumer debts every month, it’s hard to look for a better job, move across the country, or pursue your passions.

Minimized interest costs - Smart borrowing makes a lot of things possible. But consumer debts with high interest rates offer little benefit — you pay a significant amount of interest that’s gone forever. Those costs steal money from your budget and require you to earn more for the same standard of living. That’s the benefit of consolidating debt with a home equity line. Rates for home equity loans are significantly lower than trying to consolidate debt with a personal loan.

Frequently asked questions about debt consolidation

When is debt consolidation a good idea?

Debt consolidation works best when you can find an interest rate on a loan that’s considerably lower than on a credit card, or personal loan. But it all depends on both your personal financial situation and on the type of debt consolidation being considered.

When is debt consolidation a bad idea?

Sometimes a debt consolidation loan will come with higher interest rates and shorter repayment terms. If consolidating your debt is going to force you to repay your loans at a higher interest rate, you’re better off keeping your multiple loans, even if it’s frustrating.

Does debt consolidation hurt your credit?

Debt consolidation can help you lower your monthly payment and could end up improving your credit, but only if you stick to a plan to pay down your debt. On the flip side, it’ll also hurt your credit if you fail to pay back the loan.

When should I consolidate my debt?

There’s no real “ideal” time to consolidate debt. Whether you do it in March or December, the important questions to answer before pulling the trigger are:

Can you save money on interest by securing a lower monthly payment?

Can you qualify for a lower payment that would make managing your debts easier?

Are you tired of juggling multiple bills every month?