What are the types of bad loans?

So what are bad debts? Any debt that you cannot repay is considered bad debt. Bad debts are also ones that do not contribute to your net worth or depreciate in value over time.

Research shows that the average American is more than $90,000 in debt, but is this necessarily such a bad thing?

If you are unable to pay any of it back, then of course it is definitely problematic. However, some debts can add value to your financial portfolio and open up new opportunities when they are managed responsibly.

But what about the bad loans out there? Bad debts make it difficult to budget correctly and set off a vicious cycle that renders you unable to make repayments.

So what’s the difference?

For the most part, what separates the two is the interest rates that are charged and the way that you handle the debt.

Here's how to avoid bad debts and the alternatives that are available instead.

Bad debts defined

So what are bad debts?

Any debt that you cannot repay is considered bad debt. Bad debts are also ones that do not contribute to your net worth or depreciate in value over time.

These types of debts can also hurt your credit score.

When you are overwhelmed with debt or you are using too much of the debt available to you, this is also classified as a bad loan. Using too much of the debt available to you gives you a high debt-to-credit ratio (which describes the amount you owe across all revolving credit).

Examples of bad debt include payday loans, which promise you fast cash that you can repay on your next payday, but they charge high-interest rates. Other bad debts include credit cards with high-interest rates, expenses that get out of control, personal loans for discretionary purposes, and loan shark deals.

We will dive deeper into these bad loans and we’ll also talk about ‘good’ loans that actually help you to purchase big-ticket items that may be otherwise unaffordable.

Types of bad debt

Bad loans can easily spiral out of control if you do not get on top of them and create a plan to get out of debt. Ideally, it is best to avoid these types of loans altogether and instead focus on the type of borrowing that is going to contribute to your financial wellbeing. So if you want to avoid bad loans, then try to stay clear of the following:

Payday loans

Payday loans may seem tempting if you are desperate for some quick cash and it is taking too long to get a traditional loan. However, they should be your very last option, because these types of loans are infamous for their extreme interest rates, which can get as high as 391%-521%. You could be paying as much as $15-$30 dollars for every $100 you are charged.

The most notorious payday lenders may even charge double that amount, which is a sure-fire way to make bad debt worse. Additional service and late fees will often be charged on top of that in a misguided attempt to force you to pay off your loan quickly.

Loan sharks

The only lenders that are worse than payday loans are loan sharks. These types of lenders prey on the vulnerable and lure them in with promises to lend money with no background checks, or credit score needed.

Like payday loans, these types of lenders charge extremely high-interest rates and require quick repayment. Unlike payday loans, there have been cases of loan sharks resorting to violence when repayment is not received on time. If you are desperate for money, borrowing from a loan shark is likely to make your situation much worse.

High-interest credit card debt

High-interest credit cards can make it difficult to keep up with your repayments every month. As with any other loan, if you don't keep up with payments, it can negatively impact your credit score. If you have high-interest credit card debt, it is best to pay off the monthly repayments in full or consolidate this debt with a lower-interest loan.

Purchases made on credit cards are often used to pay for things that either do not add to your net worth or depreciate over time, like vacations, toys, baby strollers, and other common items.

Auto-loans

Buying a car may seem like a worthwhile purchase, but the truth is cars depreciate in value over time and it starts to go down in value as soon as you leave the lot. It then starts to depreciate more slowly over time. This is due to a number of factors like mileage, warranty length, fuel economy, changes in conditions, and service history, among other reasons.

If you are thinking of buying a car, consider buying a used car that depreciates at a slower rate. Another alternative is to lease a car, instead of buying a new one. Auto loans also come with high interest and the lower your credit score, the higher the interest rate is likely to be.

How to avoid bad debt

Breaking the cycle of bad debt can be challenging and overwhelming. The key to improving your financial circumstances is to get on top of bad debts and avoid getting into a similar situation in the future by taking the following steps:

Consolidate your debts

If you are struggling to pay off multiple loans or debts, then one option is to get a low-interest personal loan to consolidate them. This means that you pay less interest overall and reduces the number of payments you have to worry about. It can also reduce the likelihood of you falling behind on your payments because you will only have to deal with lower and fewer payments.

Pay debts in full each month

This may seem like an obvious point, but making repayments on time for existing debts can stop good debts from becoming bad debts and ensure that you are keeping on top of your payments. Timely repayments will also count towards your credit score. This can make it more likely that you will get approved for lower-interest debts, which makes it less likely that you will be tempted by bad debts, or high-interest loans when money gets tight.

Build an emergency fund

It is always a good idea to set aside some money for a rainy day. Ideally, you should save enough money to cover yourself for 1-3 months in the event that you lose your primary source of income. Building a savings fund also means that you will be better equipped to pay any emergency or unexpected expenses as and when they crop up.

Invest in your future

Focus on applying for credit that will contribute to your overall financial wellbeing. Instead of being tempted by quick cash that will cost you more in the long run, consider some of the alternatives to bad debt, like long-term loans, low-interest personal loans, and equity. All of these things can help you to cover the cost of any expenses while limiting any excessive fees or interest rates.

Alternatives to bad debts

Thankfully there are many alternatives to bad debts that will help you access the funds you need, without setting off a vicious cycle of late repayments and charges.

If you need the cash to pay for big-ticket items, consider the following:

Personal loan

One alternative to bad debt is a low-interest personal loan that doesn’t have steep interest rates. You can use a personal loan to finance a point of sale purchase, while building your credit with monthly repayments. A personal loan is often between $1,000-$8,000, so it is usually not used to cover big-ticket expenses, but it is ideal to help with day-to-day purchases. If you have several other high-interest loans, you may also be able to use a personal loan to consolidate all of these other high-interest debts, which means you will pay less interest.

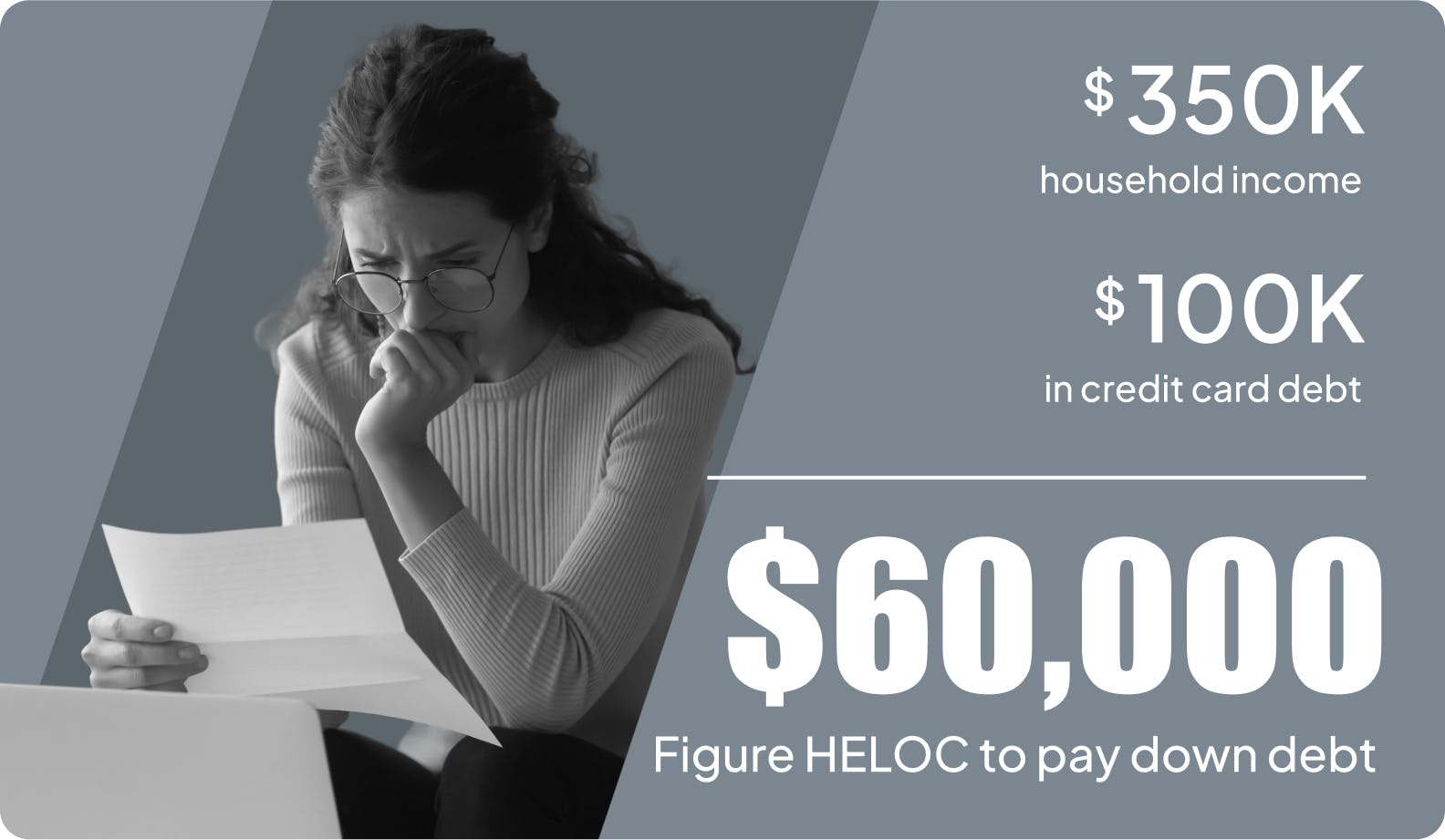

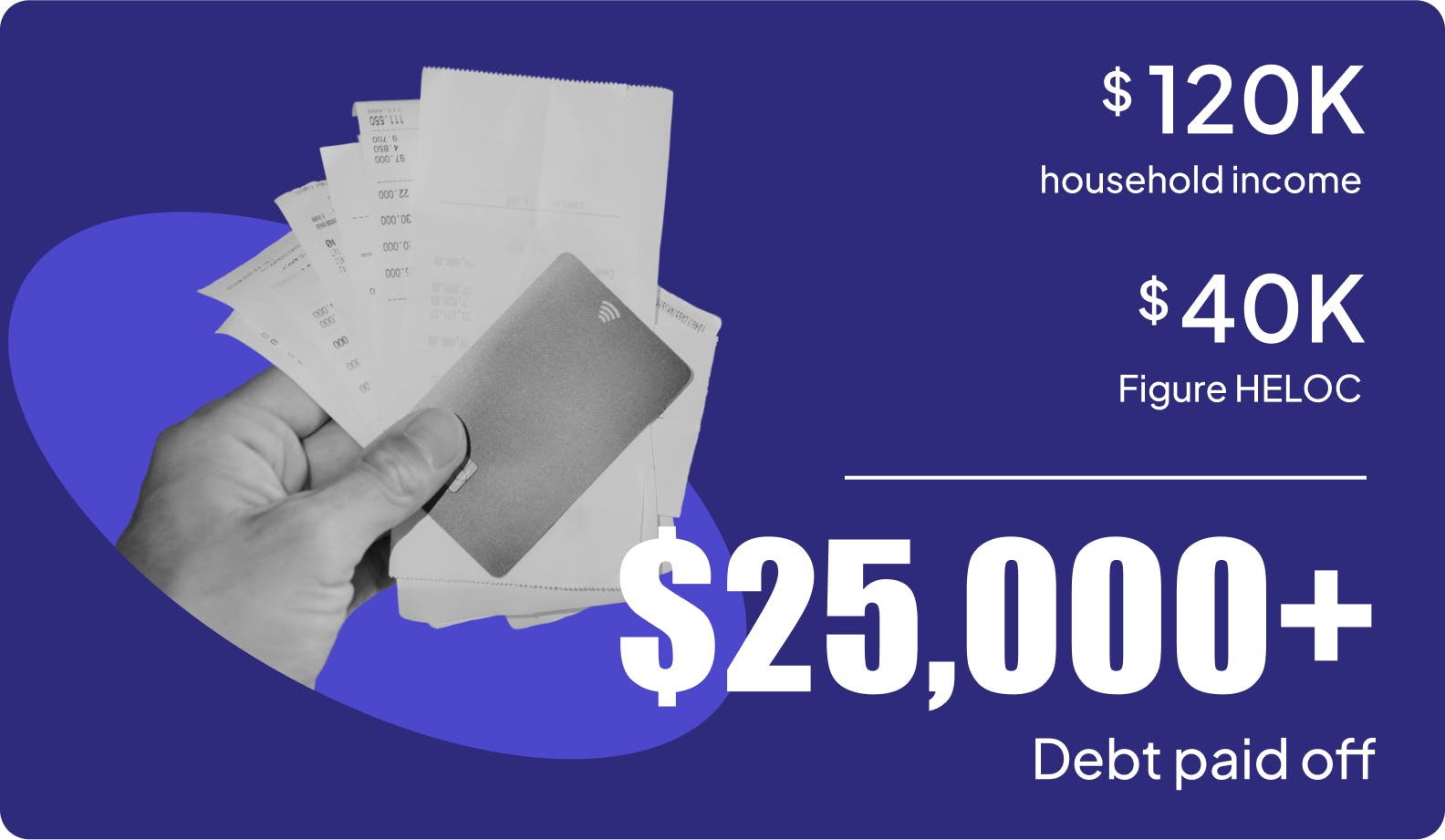

HELOC

A home equity line of credit or HELOC gives you access to a revolving source of funds, in much the same way that a credit card does. It can be used to fund big-ticket items like a home renovation, or college fund. To qualify for a HELOC, you will need a good credit rating and equity in your home. The advantage of a HELOC is you can withdraw money as and when you need it, so it is ideal in situations where there are ongoing costs and undefined expenses.

Cash-out refinance

Cash-out refinancing allows you to replace your home loan with a new mortgage that is higher than your outstanding balance. The difference goes to you in cash and is essentially a way for you to take advantage of the equity you’ve built up in your existing property. This usually comes at a lower interest rate than the mortgage you currently have.

Figure out your finances

Figure makes it easier than ever to apply for a HELOC without complicated processes and wait times. Learn more about getting a HELOC with Figure.